Global Market and Economic Perspective

Global Economic Commentary

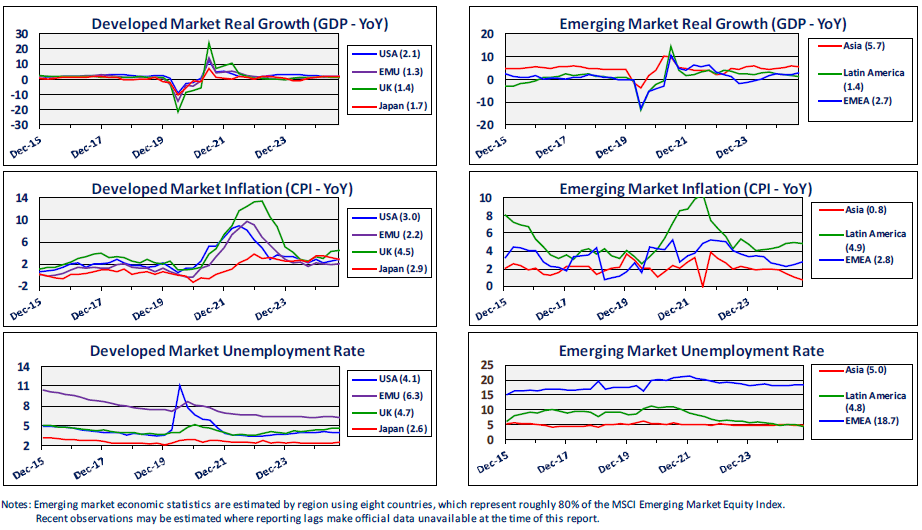

- The release of the official BEA estimate of third quarter U.S. economic growth is delayed by the government shutdown, but most other sources suggest it remained firmly around 2%, underpinned by strong consumption. Growth for the quarter in China slipped below 5% but also remained above expectations with an even more notable bifurcation between weak consumption and strong exports. Growth in other major developed markets remains around 1.5%.

- While inflation ticked up and remained slightly above targets across major developed markets, it continued to decline across Asian emerging markets to levels that are well below the average of the past couple decades. A majority of global central banks, including the FED, cut policy rates during the quarter. Both the ECB and the Bank of Japan left policy rates unchanged in line with expectations.

- Unemployment during the third quarter remained just off recent lows in most countries, with the continued observation that in the midst of a steady unemployment rate, there has been less movement than normal (with both limited new jobs and job losses) in the U.S.

Stairway Partners is an SEC-registered Investment Advisor providing comprehensive investment advice and industry-leading portfolio management solutions. Our firm was created to provide institutions and individual investors with transparent and cost-effective stewardship of their assets. Our sophisticated investment capabilities and a steadfast commitment to the industry’s best practices have allowed us to serve as a valued advisor and trusted fiduciary to clients throughout the United States. For more information, please call (630) 371-2626 or email us at stairwaypartners@stairwaypartners.com.

Global Equity and Currency Commentary

- For the third quarter, global equity markets moved notably higher across the board once again. U.S. large cap growth stocks led U.S. large cap value stocks, while small cap outperformed large cap.

- Emerging markets extended their outperformance in 2025, as they outperformed the U.S. in each of the first three quarters with consistent contributions from both local market performance and currency exposure.

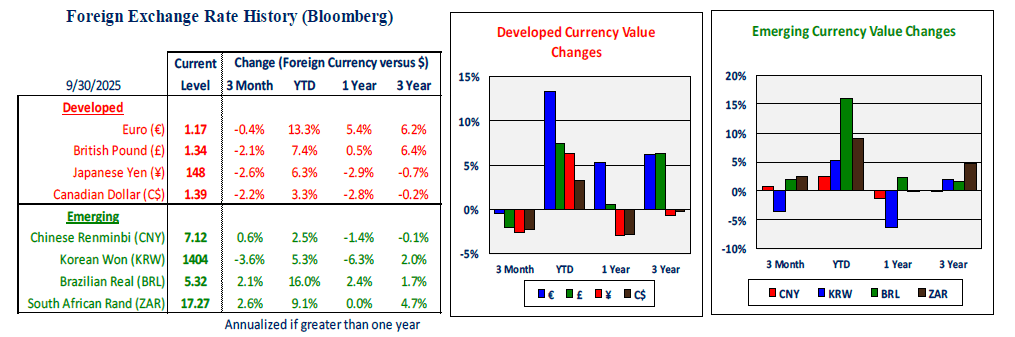

- Non-U.S. developed markets were nicely positive on an absolute basis during the quarter, but underperformed the U.S. and emerging equity markets, partly as a function of a stronger dollar. Developed markets remain well ahead year to date, with contributions from both local markets and currency.

US Fixed Income and Fed Commentary

- In the third quarter, the Treasury yield curve remained steeply upward-sloping, as yields fell relatively uniformly across maturities. The FOMC cut rates in the quarter and expectations for the budget deficit showed some early signs of stabilization.

- The decline in interest rates led to gains in other investment-grade fixed income. Corporate bonds and tax-exempt municipals performed even better than Treasuries across the maturity spectrum, as credit spreads narrowed meaningfully for the quarter.

- The FOMC’s economic forecasts shifted toward higher growth and increased inflation after recent tariff and tax policy changes. The Fed still projects reducing policy rates toward a neutral posture over the coming 12-18 months and has made additional steps in that direction after cutting rates in Q3 (and in early Q4).

Stairway Partners, LLC © 2025

This material is based upon information that we believe to be reliable, but no representation is being made that it is accurate or complete, and it should not be relied upon as such. This material is based upon our assumptions, opinions and estimates as of the date the material was prepared. Changes to assumptions, opinions and estimates are subject to change without notice. Past performance is not indicative of future results, and no representation is being made that any returns indicated will be achieved. This material has been prepared for information purposes and does not constitute investment advice. This material does not take into account particular investment objectives or financial situations. Strategies and financial instruments described in this material may not be suitable for all investors. Readers should not act upon the information without seeking professional advice. This material is not a recommendation or an offer or solicitation for the purchase or sale of any security or other financial instrument.

You must be logged in to post a comment.